How many people does it take to ship a container of avocados from Kenya to the UK? At least thirty, but more importantly, there are over 200 individual events and communications involved. Global organisations are now exploring how using blockchain technology in the supply chain can leverage their businesses and gain competitive advantage. More about how blockchain works here.

Blockchain could be a game changer in complex and cumbersome supply chains that are document-heavy. It has the potential to speed up administrative processes and to take costs out of the system while still guaranteeing the security of transactions. International trade and financial processes are the prime candidates.

The benefits

Some of the benefits that are immediately apparent are:

- More reliable and trustworthy databases

- Reduced errors in document processing

- Greater visibility of transactions for all participants

- Secure and safe auditable records

- Speedier processes leading to cost savings

Private blockchains can provide a level of confidence and security in the transfer of information on assets in the supply chain that has not been evident to date. Industries with the greatest potential are those which deal with extensive paperwork such as freight forwarding, marine shipping, and transport logistics. Other industries that are tightly regulated such as healthcare services and food distribution are strong contenders for the technology.

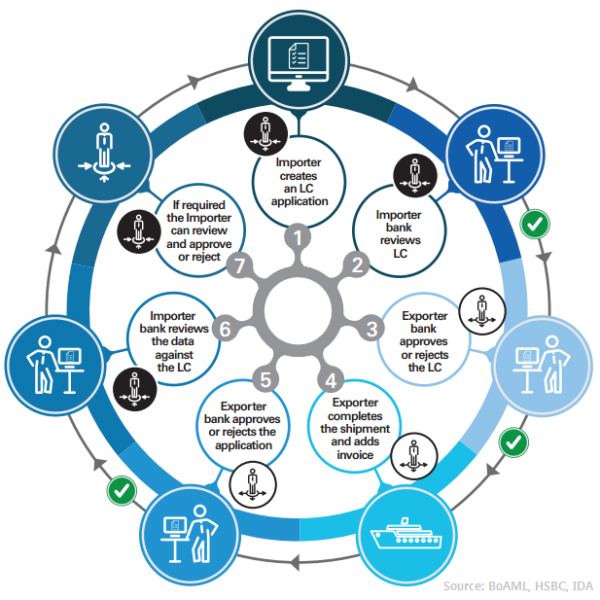

Trade Finance

This is a broad term that covers a range of activities such as letters of credit (LCs), issuing of guarantees, money transfers and insurance. The processes involved are tedious, slow and labour-intensive. Many documents are needed to provide asset assurance to sellers and buyers and to contain their risks. Major banks such as Barclays, HSBC and Bank of America are investing in blockchain start-ups. They have discovered that they can speed up their back office operations and settlements through having digitised ledgers that are secure, accessible (with appropriate user controls) and transparent.

Example: Letter of credit (LC)

Food Logistics

There is a multitude of problems in food supply chains. Food fraud where items are misrepresented and even fraudulent are common, recalls are becoming more frequent. These issues result in economic losses and damage the brand and can create health, ethical, and environmental concerns. Consumers are becoming more discerning and expect detailed information about how food is transferred “from farm-to-fork”. John West, a global producer of canned fish, views it as a competitive advantage to make its supply chain transparent. John West prints codes on their cans to allow consumers to trace the tuna all the way back to the fisherman who caught it. This innovation netted the company over $22 million in increased sales.

Last year, Walmart launched its Food Safety Collaboration Centre in Beijing. Walmart is collaborating with IBM and Tsinghua University to improve the way food is tracked, transported and sold to consumers across China by applying blockchain technology.

Pork, traditionally a delicate food product requiring tight handling in the cold chain, was chosen as the pilot. Information such as farm origination details, batch numbers, factory and processing data, expiration dates, storage temperatures and shipping detail are digitally linked to the physical food items as it moves from source to destination. As a result, each pork item received at a store is verified as authentic, and its digital record could potentially reveal food safety issues picked up between farm and store.

Healthcare

Healthcare supply chains are generally not networked to the advantage of the individual institutions involved in them. Blockchains can allow hospitals, patients, doctors and other health professionals to share access to other information networks without compromising data security and integrity. There have been some innovative start-up platforms that enable, for example, multi-signature authentication. Philips Blockchain Lab is experimenting in this area.

IBM is working with the US Food and Drug Administration on using blockchain to track use of personal health data by its Watson system, initially focusing on oncology.

The Bill and Melinda Gates Foundation is funding research to support the creation of an electronic health records system that provides immutability and security in an affordable manner. The intention is to provide a higher probability of accurate diagnoses, more effective treatments, and the overall increased ability of healthcare systems to deliver cost-effective care.

Marine shipping

Leading the way is Danish shipping company, Maersk. It is collaborating on a blockchain-based system for tracking consignments that will address visibility and efficiency. In its pilot project on shipping avocados from Africa to Europe Maersk found that moving such a shipment involved more than 200 interactions and communications. When adopted at scale, the solution has the potential to save the industry billions of dollars, says Maersk. “We expect this to not only reduce the cost of goods for consumers but also make global trade more accessible to a much larger number of players from both emerging and developed countries,” says Ibrahim Gokcen, Maersk’s chief digital officer. Original documents can be created, validated and notarized, all within the blockchain. Change of ownership midway through a shipment is made possible as well as the possibility to trace back the origin of all documentation.

Public blockchains are also being established in this industry. One is providing a permanent information source about the attributes and capacities of shipping containers for port officials, transport companies, shippers and cargo owners. This replaces cumbersome logs, spreadsheets, data intermediaries and private databases.

The Port of Rotterdam, Europe’s largest shipping port, is taking part in a Blockchain consortium which is focusing on logistics. The project has the support of more than fifteen public and private sector companies based in the Netherlands and is unique because of its scale and the participants. ABN Amro is working with Dutch university TU Delft and a host of other partners such as Royal FloraHolland and Innopay – the bank and university are focussing on three user cases: supply chain finance, inventory finance and circular economy.

Samsung is launching a pilot blockchain project for Korea’s shipping logistics industry to track imports, exports and the location of cargo shipments in real-time over a blockchain ledger. The electronics industry is commonly plagued by breakages and cargo fraud in its logistics operations. Over a shared tamper-proof ledger, the entire process of a logistics operation is made transparent, right through manufacturing, processing, storage and transportation of goods.

Automotive

Tracking of automotive parts as they move between manufacturing facilities and countries is an attractive application for blockchain. Toyota is venturing into developing blockchain solutions for their core parts supply chain operations. Interfaces between OEMs and their 3PL transport partners are complex and not well-integrated. There may be hundreds of transactions and message types where information is typically transferred across different I.T platforms, which is expensive and error-prone. Keeping accurate records, in real-time, of the thousands of parts that go into building a car would make Toyota more efficient, and could also help during supply chain disruptions. Automotive company Mahindra is also experimenting with blockchain to run its invoice discounting business.

Who is next?

The use of blockchain technology could help create more transparent and less vulnerable supply chains in certain industries that are transaction heavy.

Any industry that suffers from a lack of transparency during and after transactions, copious amounts of paperwork, possible fraud, and document errors may find a possible solution in a blockchain. Real estate has great potential due to the mass of records and documents involved. Blockchain applications can help record, track, and transfer land titles, property deeds, liens etc. and help ensure the documents are accurate and verifiable. Other future applications could include voting systems, car hire and leasing and the music industry.

So where are we now?

The possibilities are exciting but it is early days and there are some challenges looming. There is a need convince all involved parties to join a particular blockchain and collaborate for mutual benefit. Without this, it won’t work well.

The final article in this series will highlight some of the difficulties for companies wishing to consider blockchain solutions and we will find out what the innovators are up to.

Blockchain image courtesy of Kepler Consulting.